|

|

【TOPGLOV 7113 交流专区】顶级手套

[复制链接]

[复制链接]

|

|

|

发表于 21-1-2008 01:00 PM

|

显示全部楼层

发表于 21-1-2008 01:00 PM

|

显示全部楼层

原帖由 tan81 于 21-1-2008 12:32 PM 发表

我觉得我们的讨论,也许会陷入膠着的状况。

问题在于,有没有人理解手套厂的运作和实地考察。

我虽然是工程师,却未曾有机会到手套厂看过。不过有位前辈是在Kossan做的。

可以问他的意见。

对我而言,制造业有 ...

其实话虽讨论,

但是大部分时间是限于胶着的,

因为会开声发表意见的都是有着自己主见的人,

会被左右的一般只有读帖的中立份子,

所以啊,还是看戏 |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 01:03 PM

|

显示全部楼层

原帖由 tan81 于 21-1-2008 12:32 PM 发表

...

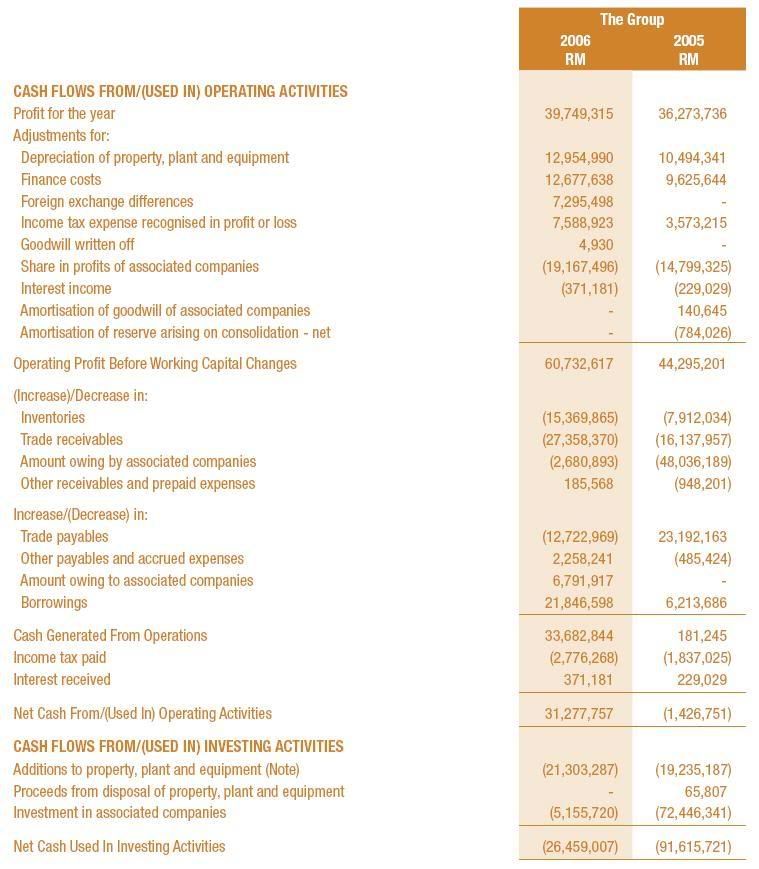

有Supermax 的 CashFlow 记录吗?

supermx 的 cashflow 应该也是 net from operation < investment。

kossan 的呢,应该是刚好平衡。

其实,这跟它们的扩充策略有关。topglov、supermx 属于激进型扩充,kossan 是稳健型。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 01:18 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 01:23 PM

|

显示全部楼层

原帖由 tan81 于 21-1-2008 12:32 PM 发表

...

对我而言,制造业有资金可以自供自给,是难于理解的。 ...

大家请搞清楚状况。

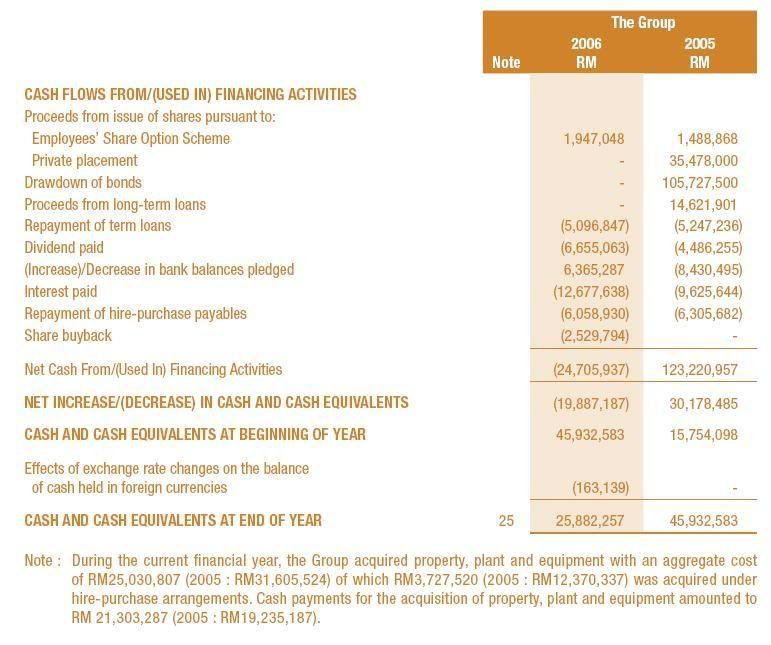

目前的 topglov是处于积极扩充状态。

这种情形下的cashflow,是跟刚刚创立公司时类似的。投入的现金必定大于营运收入。

这时候你们要求它的 cashflow自给自足,好象不太合理。

看看 topglov的数据,过去几年,它的营业额 CAGR 大约 40%。

假设它的资产回酬率不变,其 asset 增长率该要和这差不多。

如果你要求它的长期保持 operation cash > investment cash,除非:

(1) 它的 ROA 大于 40%(更正确来说,应该是 net operational cash / incurred asset 大于 40%)

(2) 放慢增长,使其增长率低于ROA。

我觉得:

(1)的情况近乎不可能。

(2)的情况不是大多数人想看到的,不过却是 topglov以后必经的阶段。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 01:28 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 01:31 PM

|

显示全部楼层

大家如此很精彩的分析,厉害,真是佩服了

之前的 PRIVATE PLACEMENT 会不会是因为有计划要买橡胶园才发出的, 而最后又因为价钱太高而暂时搁置了.

顶级依然是一间还有在赚钱的公司而且又有成长, 对于未来的资金应该是不会有问题吧?

至于回购股票呢,早期的 IOI 与 PBBANK 也是有强力的回够过股票,那时候很多基金都在抛售他们 ,而回购都是在15/16 以上的本益比,顶级还是一间有成长的公司,PE 是比较难跌到12 或 10 以下吧,不过也是很难讲,因为在马来西亚是会比较缺少外资的资金的. |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 01:44 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 01:51 PM

|

显示全部楼层

回复 928# 的帖子

|

压根儿都不提和美国Tillotson的纠纷。Supermax和它的协议如果延伸到全球市场,没有理由Topglov只放弃美国市场就没事。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 06:48 PM

|

显示全部楼层

Top Glove现在形势不好。。。这个时候就要看谁的耐性比较好了。。。

| Notice of Shares Buy Back - Immediate Announcement | | Reference No CS-080121-83810 |

| Company Name | : | TOP GLOVE CORPORATION BHD | | Stock Name | : | TOPGLOV | | Date Announced | : | 21/01/2008 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 07:35 PM

|

显示全部楼层

今年不是出口年。。。

21-01-2008: Strengthening ringgit to squeeze semicon players

by Sharmila Ganapathy

KUALA LUMPUR: The continuing appreciation of the ringgit against the greenback will squeeze profit margins of export-heavy Malaysian electronics firms, particularly semiconductor players.

Analysts are expecting a contraction in end-user electronics sales this year, with the US recession and global economic slowdown looming in the horizon.

Global research firm Gartner Inc forecasts worldwide semiconductor equipment spending will fall 9.9% to US$40.3 billion (RM133 billion) this year across all segments, including wafer fab, packaging and assembly and automated test equipment.

Think-tank Malaysian Institute of Economic Research (MIER) last week forecasted that the ringgit would eventually touch 3.00 to a dollar this year.

The strengthening ringgit, coupled with slowing retail electronics sales, will impact local electronics firms, analysts said.

“Power management and communication chip companies will be severely impacted,” said an analyst at RHB Research Institute Sdn Bhd.

“The semiconductor market will pick up in the first half of the year due to demand from China for displays and communication devices for the Beijing Olympics, but it will be short lived,” he said.

However, post-Olympics, the Chinese government could increase rates to curb inflation, hence consumer spending is expected to decline after the Olympics, he added.

One company that will be hit hard by the appreciating ringgit is Malaysian Pacific Industries Bhd (MPI), said an analyst with a bank-backed research house. “The company’s entire revenues are US dollar-based, while only 30% of its costs are ringgit-denominated, he said.

“Additionally, its operations in China are not enjoying the kind of cost advantages it should, because it is looking at coastal areas. Its costs in China are fairly comparable with its operations here in Malaysia,” he added.

A CIMB Research report last November said MPI was making efforts to cut costs by spending on equipment to enhance productivity and discontinuing lower-end products.

“MPI is largely constrained from raising selling prices as there is little product differentiation from its competitors,” CIMB said in the report.

Local firms tied to US-based chip manufacturer Intel Corporation will also be impacted. Intel shares fell 12% last Wednesday after reporting weaker 4Q results.

“We see automation firms like Pentamaster Corporation Bhd and LKT Industrial Bhd impacted by Intel trimming its expenses,” the RHB Research analyst said.

Uchi Technologies Bhd, which exports coffee modules that control coffee machines, will also see its earnings hurt. “A 1% fall in the US dollar would cause Uchi’s earnings to fall 1.7%,” he said.

The analyst with the bank-backed research house agreed that Uchi’s earnings would be marred by the ringgit appreciation.

“Its coffee modules unit growth is still strong. However, it remains to be seen if it is able to price in the strengthening ringgit into its new and existing contracts,” he said.

Another company to feel the pinch of the firming ringgit, though at a lesser extent, will be Unisem Bhd. The semiconductor packaging player will feel an earnings bite although demand remains strong for its products.

“We don’t see a slowdown in growth prospects and earnings. AIT (Advanced Interconnect Technologies) is a good acquisition and will drive their growth. Their business in China will also help mitigate the impact of the currency mismatch,” the analyst said.

The RHB Research analyst meanwhile said Unisem’s independent wafer bumping services also put it in good stead.

He added that Globetronics Technology Bhd was also expected to fare better than many of its peers. |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-1-2008 07:43 PM

|

显示全部楼层

原帖由 留下眼镜 于 21-1-2008 01:51 PM 发表

压根儿都不提和美国Tillotson的纠纷。Supermax和它的协议如果延伸到全球市场,没有理由Topglov只放弃美国市场就没事。

请问你清楚美国Tillotson的纠纷是何回事吗? Topglov现在照样可以出口Nitrile手套去美国的。。。

Malaysian, Indonesian Glove Companies Contest Tillotson's Patent Claim

By Kristy Inus

KUALA LUMPUR, Aug 1 (Bernama) -- Seven Malaysian and one Indonesian glove producers have teamed up to contest US-based Tillotson Corp'sclaim that there has been a patent infringement by the companies on nitrile gloves exported to the U.S.

There is a possibility that more companies will join the group.

The joint committee inclusive of Malaysian's Top Glove Corp Bhd,Hartalega Holdings Bhd, Kossan Rubber Industries Bhd, Laglove (M) SdnBhd, Riverstone Resources Sdn Bhd, Smart Glove Holdings Sdn Bhd, YTY Holdings Sdn Bhd and Indonesia's PT Shamrock Manufacturing Corp, is making its move through the Malaysian Rubber Glove Manufacturers Association (MARGMA).

"We hope to group more (companies) to counter Tillotson's claims and the U.S. lawyers we've engaged have already put things into action.

"We want to invalidate the patent, and will make our stand based on arguments why we do not think the patent is valid," Top Glove executive director K.M. Lee told Bernama when met at a mock-cheque presentation here, today.

Tillotson Corp lodged a complaint with the U.S. International Trade Commission (ITC) on May 30, requesting investigation into possible intellectual property infringement among 30 global nitrile glove manufacturers, dealers and importers, including more than 10 Malaysian companies.

The U.S company is asking US$2 royalty for every 1,000 nitrile gloves imported into the U.S.

Before this, Top Glove which is the world's largest rubber glovemaker, has already said that it was expecting no material implications to its financial results from the allegations. Its nitrile glove salesto U.S. makes up less than three percent of its total turnover.

"I also want to clarify that Tillotson did not actually win all the previous suits as reported ... Most of these cases were not actually taken to court and they were settled outside through voluntary agreements," Lee said.

"With a big number in our group, I believe we can succeed in the contest against the claims," he added.

A case like this could take up one and a half years before settlement but with the nearing expiry date for Tillotson which claims the US patent for nitrile gloves until 2010, a positive outcome isexpected.

When ITC makes a decision, it will also not affect the company as no backdated payments are expected to be made, Lee added.

-- BERNAMA

[ 本帖最后由 Mr.Business 于 21-1-2008 07:46 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 01:52 AM

|

显示全部楼层

回复 932# Mr.Business 的帖子

|

你很爱名,人家股友是拿真金白银来投资的,总要对他们有一点责任感。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 08:06 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 08:22 AM

|

显示全部楼层

origen兄介绍的博客文章。。。

Not-So-Top Glove

Business Times - The world's biggest manufacturer of rubber gloves, Top Glove Corp Bhd, has set aside RM100 million this year to buy a rival and expand its factories. Currently, TG produces 29 billion pieces of gloves a year, which is about 24 per cent share of the global market. It aims to capture 35 per cent by December 2010. The estimated annual demand by then is 160 billion gloves. Cheong Guan, who is also the finance director, said that TG expects to boost its net profit by 22 per cent to RM125 million for the fiscal year to August 31 2008. TG is also confident that a slowing US economy will not affect its business because rubber gloves are a necessity.

Caveats:

1) A slowdown is a slowdown, how not to be affected. 30 per cent of TG sales comes from the US, rubber gloves.

2) Patent suit pending - Even though the company is optimistic of winning.The reality may indicate otherwise. On May 30 last year, the US-based Tillotson Corp filed a complaint against all nitrile glove manufacturers, distributors or importers worldwide, claiming to be the patent holder for nitrile gloves until 2010. Eight glovemakers, through the Malaysian Rubber Glove Manufacturers Association (Margma), are contesting Tillotson's claim. TG is part of the group. However, Supermax Corp Bhd, which is not part of the group, has agreed to settle and pay royalty to Tillotson.

3) TG has been able to offset USD weakness by raising prices: not going forward in a slowdown.

4) Latex prices still pushing higher putting pressure on margins.

5) Net cash per share only 33 sen and will go to 24 sen next year.

6) Capacity being boosted by 25% p.a. in 2008 and 2009, more stock going into a down cycle.

7) Reduction of tax rebates for China exports will hurt expansion business model.

8) Its gearing is low as its acquisition spree has been funded by new shares, however that creates a huge free float of about 60% with many substantial shareholders of previously acquired companies. They won't be sitting around waiting for the grand master plan to pan out.

9) Net cash flow is about only RM10m in 2008 and is projected to jump to RM50m in 2009. Still a projection with many variables.

10) Receivable is about 15%, watch for danger signs if it gets closer to 20%.

11) Looking for rubber plantations hints at margin pressures. Looking to do share buybacks hints of even bigger problems.

http://malaysiafinance.blogspot.com/ |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 08:48 AM

|

显示全部楼层

回复 934# Mr.Business 的帖子

回答像林博士。

我也谢谢,就是因为看到你为Topglov尽说好话,觉得不对路,所以才卖出。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 08:51 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 10:16 AM

|

显示全部楼层

|

现在RM5.30了。看看TOPGLOVE浪费了多少钱? |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 12:33 PM

|

显示全部楼层

应该是公司自己在顶着。。。

TOPGLOV

(7113) 12:33:20

Last Done 5.500

Change -0.100

Day High 5.550

Day Low 5.300

Best Buy 5.400

Best Sell 5.500

Volume(Lot) 1928 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 04:42 PM

|

显示全部楼层

写给 topglove 的信

Hi,

I am a small shareholder of TopGlove. As I know, TopGlove has been

doing share buy back every day for close to 2 months. Is it wasting our

money for this action? Why not use the money in proper way like

expanding the business and others? Is the management more concern about

the share price rather than the business? I just curious on the action

of share buy back. Thanks and goodday.

Best regards,

chengyk

回复:

Thank you for your email.

The purpose of the share buy back is to stabilize the supply and demand

of Top Glove's shares in the open market and thereby support its

fundamental value. Top Glove is using the surplus cash to buy back the

shares.

Share buy back is part of the corporate exercise of a listed company but

Top Glove will not lose its main focus on its main business, which is

manufacturing of gloves, which can be seen from its latest result, where

the group continues to grow by 20%.

We thank you for your suggestion.

Best regards

The Investor Relation Team

我想应该是我问的问题不太好 !!!! 答案很表面 !!! |

评分

-

查看全部评分

|

|

|

|

|

|

|

|

|

|

|

发表于 22-1-2008 04:50 PM

|

显示全部楼层

回复 940# 的帖子

Top Glove的email address是?

你应该讲你很不爽,看他有什么回应? |

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

2065

2065  132

132